Arizona’s weather is unlike anywhere else in the country. With sweltering summers, violent monsoon storms, dust clouds that can block out the sun, and large elevation swings from Tucson to Flagstaff, the state’s environment constantly tests both vehicles and drivers. These conditions don’t just wear down your car — they also shape what you pay for insurance. Understanding how Arizona’s climate affects car insurance rates helps drivers see where those costs come from and what they can do to control them.

Arizona’s Extreme Climate: The Hidden Factor Behind Insurance Costs

Arizona drivers pay unique insurance rates not just because of population or accident statistics, but also because of how weather increases the likelihood of claims. Insurance companies look at historical data for each ZIP code — including how often weather leads to vehicle damage or collisions — when setting premiums. In a state that sees record heat, heavy rainstorms, and blowing dust, those risks add up quickly.

Heat: The Constant Threat to Arizona Vehicles

Summer heat is the most persistent and damaging weather element in Arizona. When temperatures climb past 110°F, the stress on vehicles rises dramatically. Tires expand and wear faster, rubber seals dry out, and batteries lose life at double the rate compared to cooler climates. Cooling systems work overtime, and when a hose or radiator gives out, it often leads to costly engine repairs or even total failure.

From an insurance perspective, this constant strain matters. While most mechanical failures aren’t covered under standard policies, breakdowns caused by overheating can lead to accidents or roadside incidents that insurers must pay for. A sudden tire blowout or stalled engine on a busy freeway can easily result in a claim. Over time, the data from thousands of these incidents pushes rates higher in hotter regions like Phoenix and Yuma than in cooler mountain areas.

The Role of UV Exposure and Interior Damage

Ultraviolet radiation in Arizona’s desert sun doesn’t just tan skin — it fades paint, cracks dashboards, and weakens plastic trim. Although cosmetic wear isn’t usually covered by insurance, vehicles that deteriorate faster lose resale value and are more likely to develop failures in seals, electronics, and airbags. Insurers recognize that environmental wear accelerates overall depreciation, and they account for that in the cost of comprehensive coverage.

Drivers who protect their vehicles by parking in shade or using UV-resistant coatings may not see a direct premium discount, but keeping the vehicle in better condition reduces the likelihood of claims and helps preserve its insurable value.

Monsoon Season: When the Desert Turns Dangerous

Every summer, monsoon storms roll through Arizona with intense rain, wind, and lightning. Streets that were bone dry an hour earlier can flood in minutes. Drivers often face walls of dust followed by flash floods — two extremes that challenge visibility and traction alike.

Water Damage and Flash Floods

Comprehensive insurance covers weather-related damage such as flooding, hail, and falling debris. During monsoon months, those protections become essential. Even a few inches of standing water can disable modern vehicles, ruining electronics and seizing engines. Because water damage often results in total loss, insurers categorize certain flood-prone zones as high-risk. Drivers in those areas typically pay slightly more for comprehensive coverage, reflecting the higher likelihood of claims.

One of the most common claim types in Arizona during monsoon season comes from vehicles swept off flooded roads. Despite repeated safety campaigns, “turn around, don’t drown” warnings go unheeded every year. Insurers see patterns in those losses and price coverage accordingly, particularly in low-lying neighborhoods or rural washes where flash flooding is frequent.

Wind, Hail, and Flying Debris

Monsoon winds can easily exceed 60 mph. Combined with blowing sand, falling branches, or debris from construction sites, that creates constant risk for vehicle exteriors and windshields. Arizona leads the nation in windshield replacement claims, largely due to debris and gravel damage during storm season. Even small cracks can turn into large fractures from heat expansion, prompting drivers to file comprehensive claims.

Hail, though less common than in the Midwest, can still cause extensive denting and broken glass. Insurers anticipate these periodic spikes in claims and adjust premiums for regions where storm severity is highest — typically in southern and central Arizona.

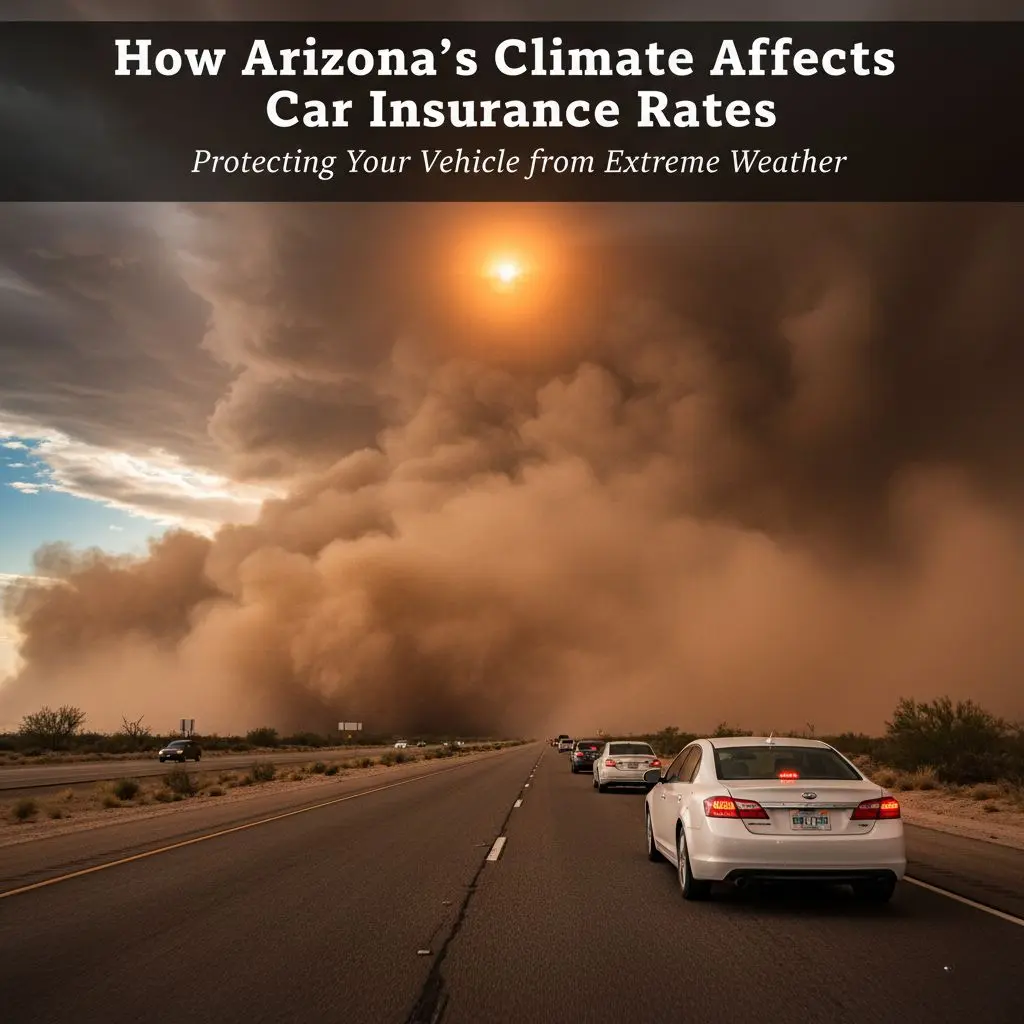

Dust Storms and Visibility Hazards

Few natural events are as sudden or as dangerous as an Arizona dust storm, locally known as a “haboob.” These walls of dust can stretch for miles, reducing visibility to zero in seconds. Drivers caught in a haboob may lose sight of the road entirely, leading to multi-car pileups that can involve dozens of vehicles.

Collision Risks During Dust Storms

Insurance companies categorize dust storm accidents under collision coverage because they often involve contact with other vehicles or stationary objects. The problem isn’t just visibility — fine dust also infiltrates air filters and sensors, causing engines to stall or misfire. If that failure leads to an accident, the result is an insurance claim that adds to regional loss statistics.

Because Arizona experiences these events every year, insurers track their frequency and severity closely. Regions most prone to dust storms, such as Pinal and Maricopa counties, often carry higher average collision premiums than northern areas of the state.

Preventing Dust-Related Damage

Drivers can lower their risk — and indirectly their future premiums — by maintaining filters, checking seals, and pulling off the road safely during storms. Turning off lights once stopped is a recommended safety practice to prevent rear-end collisions from drivers who mistake stationary lights for moving vehicles. Although insurance can help recover costs after damage, avoidance remains the best protection.

The Hidden Impact of Wildfires and Smoke Damage

While Arizona’s desert image often overshadows it, wildfires are a growing threat, especially in forested and high-elevation areas. Fires can destroy property directly or coat vehicles with ash and acidic residue that corrodes paint and mechanical components.

Comprehensive coverage typically protects against fire damage, but smoke and ash can create gray areas. Claims adjusters must determine whether the damage was sudden and accidental or gradual. For this reason, insurers sometimes see increased claim disputes following major wildfire seasons. Maintaining good photo records of your car’s condition and cleaning it promptly after exposure can strengthen a claim if needed.

How High Elevation Alters Vehicle Performance — and Insurance Risk

Not all of Arizona’s terrain sits at desert floor level. Cities like Flagstaff and Prescott are several thousand feet above sea level, with cooler air but thinner oxygen. High elevation introduces its own challenges, particularly for vehicles that have been damaged in an accident.

Engine and Brake Stress at Altitude

Thinner air means engines produce less power, forcing them to work harder on steep grades. If the air intake, exhaust, or turbo system was damaged in a collision, that reduced oxygen makes the problem worse. Similarly, brakes endure greater strain on mountain descents. A compromised brake system that performs acceptably in flat terrain might fail under sustained downhill pressure.

Insurance companies and repair shops in high-elevation areas often perform more extensive diagnostics to ensure vehicles are safe post-repair. More complex repairs mean higher costs, which indirectly influence local insurance pricing.

Tire and Cooling System Effects

Elevation changes affect air pressure inside tires. A car with minor suspension or alignment damage may develop uneven wear or instability as the elevation shifts. Cooling systems are also vulnerable: damaged radiators or hoses can lead to overheating during long climbs, even in cooler mountain climates.

Because these conditions reveal weaknesses that may not appear immediately after an accident, repair facilities like Heck’s Collision emphasize full post-repair calibration and use of OEM parts. Insurers value that thoroughness since it reduces repeat claims or mechanical failures related to incomplete repairs.

How Insurers Use Climate Data to Set Rates

Every insurance company relies on historical loss data to calculate risk. In Arizona, that data clearly shows a link between weather and claims frequency. Claims spike during the summer months, not only because of increased driving but also because of environmental stress on vehicles. High heat, dust storms, and heavy rain create conditions where more accidents and damage occur.

Climate-Driven Risk Factors

Insurers look at several weather-related variables when setting rates:

- Storm frequency: Areas with more monsoon or hail events face higher comprehensive premiums.

- Heat-related breakdown claims: Though mechanical failures aren’t covered, accidents caused by them are.

- Windshield and debris damage rates: High claim counts raise regional averages.

- Wildfire exposure: Zip codes near fire-prone forests may carry slightly higher comprehensive costs.

- Elevation effects: Mountain regions where performance and braking issues occur after repairs see more scrutiny in claim evaluation.

Over time, these localized statistics create a pricing map across the state. Drivers in hot, low-lying regions with frequent storms typically pay more than those in cooler or less storm-prone zones.

What Drivers Can Do to Reduce Risk and Cost

Arizona drivers can’t control the weather, but they can manage how it affects their vehicles and insurance costs. Preventive maintenance and smart coverage choices make a measurable difference.

Keep the Vehicle in Top Shape

Regular inspections prevent small issues from becoming claim-worthy failures. Check coolant, battery terminals, hoses, and tires before peak summer. Replace air filters often, especially after dust storms. Proper tire inflation is critical in desert heat — underinflation causes blowouts, and overinflation accelerates wear.

Wash and wax the exterior to protect paint from UV damage and remove corrosive dust or ash. Using a windshield sunshade or ceramic tint helps preserve the interior and prevent cracking. These measures reduce depreciation and keep your vehicle safer on the road.

Choose Coverage That Matches Arizona’s Risks

The minimum liability coverage required by law won’t help if your own car is damaged by weather. For most Arizona drivers, comprehensive coverage is essential because it protects against flood, hail, fire, and falling debris — all common in the state.

Collision coverage is equally valuable if you drive during monsoon or dust storm season, when accident risk rises sharply. Mechanical breakdown insurance or extended warranties can fill the gap for failures caused by heat stress, although they’re separate from standard policies.

When choosing deductibles, balance affordability with practicality. A higher deductible lowers monthly premiums, but you’ll pay more out of pocket after a storm or flood. Drivers who live in areas prone to weather events often find moderate deductibles the best compromise.

Park Smart and Plan Ahead

Whenever possible, park in covered or shaded areas. Garages, carports, or even fabric sun shelters reduce exposure to UV and heat. Avoid street parking under trees during monsoon season, where falling branches are common.

During dust storms, pull completely off the road and turn off your lights to avoid being rear-ended. In flood-prone areas, never attempt to cross running water — both for safety and because many insurers may deny claims if the driver ignored posted flood warnings.

Shop Around and Ask About Discounts

Insurance companies vary in how they weigh environmental risk. Some place heavier emphasis on storm damage, while others reward safe driving and good maintenance history. Shop for quotes periodically, and ask about available discounts for things like anti-theft devices, low mileage, or bundling auto and home policies.

How Maintenance and Documentation Protect You in a Claim

A well-maintained car isn’t just safer — it strengthens your position if you ever file a claim. Insurers often investigate whether damage resulted from sudden weather events or from gradual neglect. Keeping maintenance receipts, repair records, and periodic photos of your car’s condition can make the difference in whether a claim is approved quickly or delayed.

After an accident or weather event, take photos immediately and contact your insurer before making repairs. If you suspect hidden damage — especially after flooding, hail, or a high-elevation drive — ask for a detailed inspection. Prompt reporting prevents small issues from turning into costly disputes.

Elevation, Climate, and the Future of Car Insurance in Arizona

As Arizona continues to grow, climate patterns are shifting. Monsoon seasons have become more unpredictable, wildfires more frequent, and heat records more common. Insurers constantly update their models to reflect these changes. Some may begin offering climate-specific endorsements or adjusting premiums seasonally, similar to flood-prone states.

Electric vehicles introduce new variables, too. Their battery systems react strongly to heat, and cooling failures can be expensive. Insurers are studying long-term data to refine rates for EVs in hot regions like Arizona.

For drivers, the takeaway is clear: weather and geography aren’t just background factors — they’re core elements shaping every insurance policy in the state.

Conclusion

Arizona’s breathtaking landscapes and sunny weather come with a price: constant environmental stress on vehicles. From the scorching heat of the Sonoran Desert to the thin air of mountain highways, every climate element plays a role in how insurers calculate risk and set premiums.

Extreme temperatures wear down parts faster, monsoons and dust storms increase accident likelihood, and elevation changes reveal hidden damage after collisions. Insurance companies respond by adjusting rates to match those realities.

For Arizona drivers, the best strategy is proactive care — maintaining vehicles diligently, understanding what each coverage type protects, and choosing policies that reflect local risks. With the right maintenance habits and coverage in place, you can keep both your car and your insurance costs steady, no matter what the Arizona sky brings next.